This report comes as an effect of a need we had for many years now, that is a need which we know founders feel it too, namely to have a common understanding of the state of Romanian-born early stage startups.

Overall, the report provides valuable insights into the Romanian early-stage startup ecosystem. It highlights the prevalence of repeat founders, the importance of product validation, and the diverse range of industries and business models being pursued. It also reveals the challenges faced by startups in securing funding.

“Starting this year we’re entering a new stage with Launch Romania – uniting the next generation of groundbreakers. By this we mean fostering the entrepreneurial culture across key pillars of Romania’s future development – students, researchers and founders. In completing the landscape of knowledge and resources dedicated to the progress of Romania’s innovation landscape we’re publishing the newest edition of our annual report – The State of Romanian-born Early Stage Startups – by now a landmark piece of information for the national ecosystem and its stakeholders and which you can enjoy here. Such movements can only take place in a community designed project such as Launch Romania, powered by BCR with the support of Google and founding partner How to Web.”

Andrei Cojan | Head of Community, Launch Romania

The survey we applied for the data collection purpose was aimed to let founders’ personal experience unveil the reality that they and their peer startup founders share.

We consider a breakthrough moment to have a clearer picture of the reality founders live in by looking at various dimensions of a founder’s journey – product building, team formation, bootstrapping, sales, marketing, fundraising, hiring, scaling, and everything in between.

“We all needed to take this deep-dive into the reality of Romanian-born early stage startups. Why? Because now more than ever it’s important to tune in to what founders have to say in order to understand the problems and challenges they’re facing and therefore do our best to better support their endeavors from the beginning and therefore increase the likelihood of building innovation.”

Ionut Stanimir | Director of Marketing and Communication, BCR

“Romanian-born early stage startups and the Romanian startup ecosystem represents one of the main catalyzers of innovation, significantly impacting Romania’s economic growth. Google’s mission is to support local startups by supplying advanced technologies, knowhow and resources needed to grow and scale globally. Having alongside our journey partners such as Launch thus creating a proper space for Romanian founders of early stage startups to grow.”

Silvia Carasel | Marketing Project Manager, Google

When looking at founders we see them as holders of creative energy and its potential to innovate. In Drew Houston’s (CEO of Dropbox) words, they are the ones that found their “tennis ball”. Below is an excerpt from the commencement address by Drew for MIT’s 147th Commencement held June 7, 2013:

“I was going to say work on what you love, but that’s not really it. It’s so easy to convince yourself that you love what you’re doing — who wants to admit that they don’t? When I think about it, the happiest and most successful people I know don’t just love what they do, they’re obsessed with solving an important problem, something that matters to them. They remind me of a dog chasing a tennis ball: their eyes go a little crazy, the leash snaps and they go bounding off, ploughing through whatever gets in the way. I have some other friends who also work hard and get paid well in their jobs, but they complain as if they were shackled to a desk. The problem is a lot of people don’t find their tennis ball right away. Don’t get me wrong — I love a good standardised test as much as the next guy, but being king of SAT prep wasn’t going to be mine. What scares me is that both the poker bot and Dropbox started out as distractions. That little voice in my head was telling me where to go, and the whole time I was telling it to shut up so I could get back to work. Sometimes that little voice knows best. It took me a while to get it, but the hardest-working people don’t work hard because they’re disciplined. They work hard because working on an exciting problem is fun. So after today, it’s not about pushing yourself; it’s about finding your tennis ball, the thing that pulls you. It might take a while, but until you find it, keep listening for that little voice.”

On this note, we summon you all to go find your tennis ball; now more than ever the world needs you to find it as this is key to solving so many pressing problems the world is faced with.

This stands also as a reminder to us all, backers and supporters of founders and their endeavors as we’ve got one mission and one mission only – help them find their tennis balls.

“Over the past 14 years, How to Web has been contributing to nurturing the Romanian and regional tech entrepreneurship and innovation scene. It has accelerated the adoption of startup culture through events, programs, knowledge sharing, and activities tailored to support entrepreneurs in their pursuit of success. Launch Romania facilitates access to vital resources and connections for individuals viewing entrepreneurship as the next step in their professional journey. The report’s data informs us about the founders’ challenges and connects us to the reality on the ground – essential to any builder and to anyone building projects meant to help entrepreneurs progress.”

Monica Zara | Co-Founder & Head of Conference, How to Web – founding partner of Launch Romania

Andrei Cojan & Alexandru Agatinei | How to Web, founding partner of Launch Romania

Mara Ilie | University of Gdansk, Abel Aioanei | Dreamdata, Monica Zara | How to Web – founding partner of Launch Romania

The key findings of the State of Romanian-born Early Stage Startups Report 2024 are as follows:

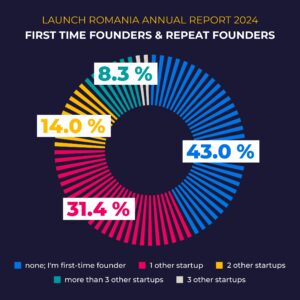

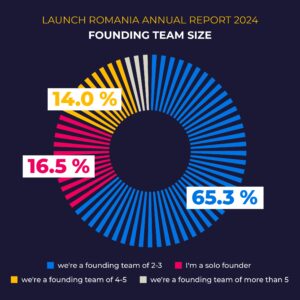

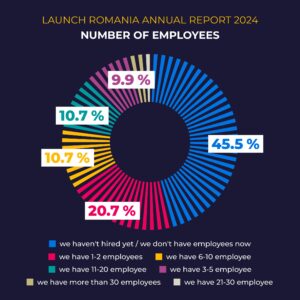

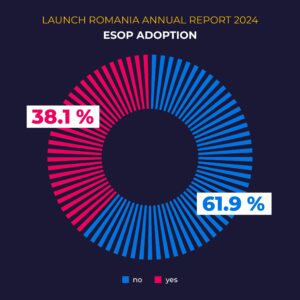

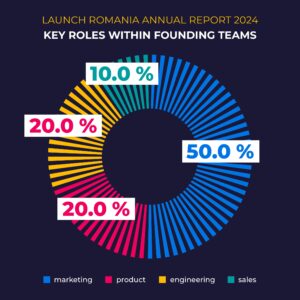

Founding & team:

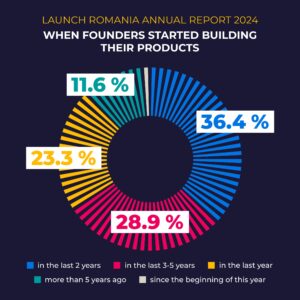

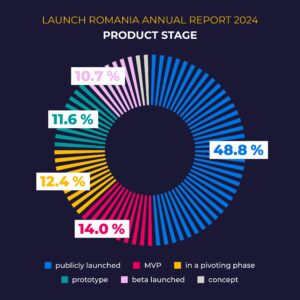

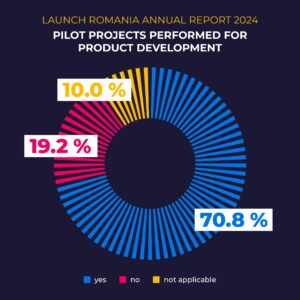

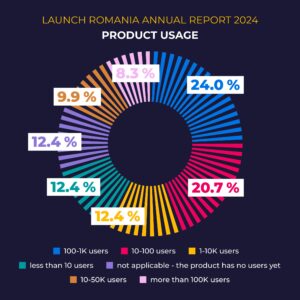

Product & Traction:

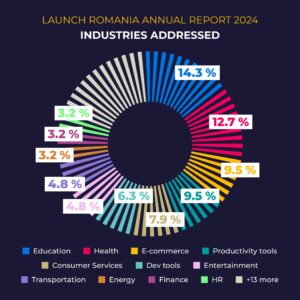

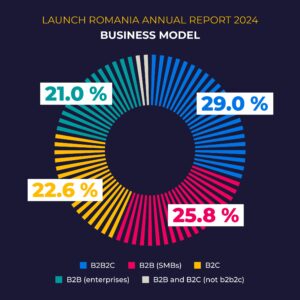

Industry & Business Model:

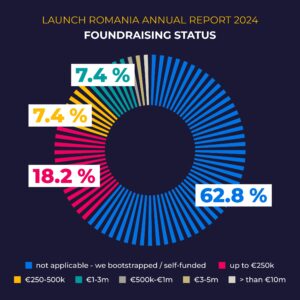

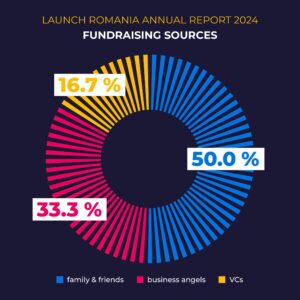

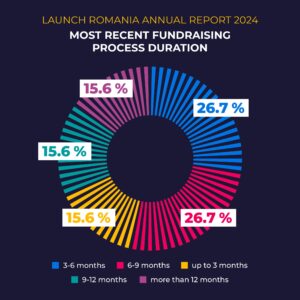

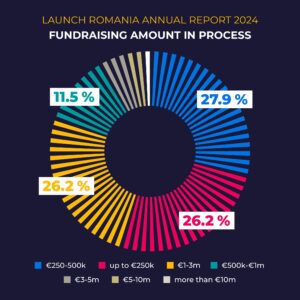

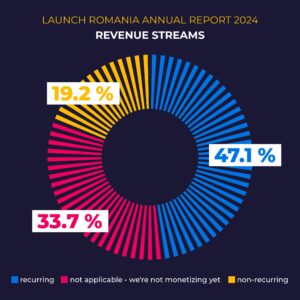

Funding & Revenue:

Launch Romania powered by BCR with the support of Google and founding partner How to Web is uniting the next generation of groundbreakers. By this we mean fostering the entrepreneurial culture across key pillars of Romania’s future development – students, researchers and founders.

Find more about BCR here

Find more about Google here

Find more about How to Web here

It is important to note that this data is based on a specific sample of startups and may not be representative of all early stage startups in Romania. Throughout the data collection process we received north of 200 survey responses from founders of Romanian-born early stage startups.

By Romanian-born we mean that from a founding team perspective all or at least the majority of the founding team members have Romanian roots.

By early stage startups we take into account the following: